A mutual fund is an investment vehicle that invests across asset classes and is used as a source of wealth preservation as well as wealth creation. To make the most out of mutual funds, choosing the right scheme that suits one’s goal and risk appetite is important. And, when it comes to choosing a mutual fund scheme based on the investment mechanism and distribution of gains, an investor has two options – Growth and IDCW plans (formerly known as Dividend Plans).

GROWTH PLANS

A growth plan is a cumulative option where the gains earned through dividends or the sale of the stock holdings continue to remain invested in the scheme instead of being paid out to the investors.

IDCW PLANS (INCOME DISTRIBUTION CUM CAPITAL WITHDRAWAL PLAN)

In IDCW plans, gains earned by a mutual fund scheme are declared as dividends at pre-decided intervals. Fund houses offer various schemes ranging from monthly IDCW plans to yearly IDCW plans, which could be chosen according to an individual’s preference.

TYPES

IDCW Plan – The dividends are declared at pre-determined intervals and paid out to the investors.

IDCW Reinvestment Plan – The dividends are declared at pre-determined intervals but are re-invested into the scheme.

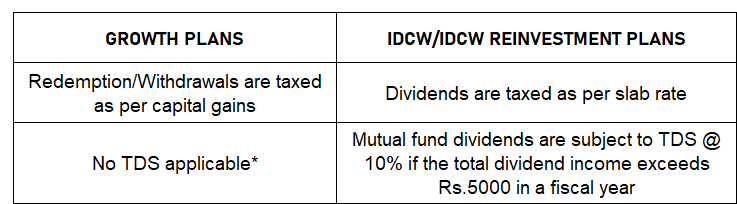

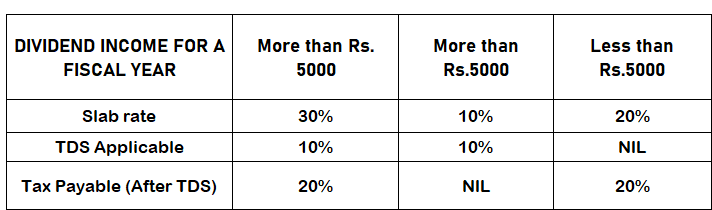

In both IDCW and IDCW Reinvestment plans, investors are taxed at their respective slab rates when dividends are declared. Investors might confuse the IDCW reinvestment plan with the growth plan, unaware of the tax applicability as the gains are reinvested into the scheme.

For example, if your dividend income is more than Rs.5000 and you fall under the 30% tax slab, after deducting 10% TDS, you’ll have to pay 20% tax.

If you fall under the 10% tax slab, then you need not pay any tax after TDS.

If you fall under the 20% tax slab and if the dividend income is less than Rs.5000, then you’ll have to pay 20% tax.

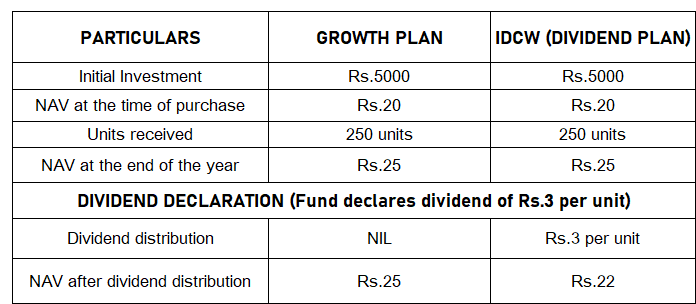

HOW DO DIVIDEND DECLARATION AND DISTRIBUTION AFFECT THE NET ASSET VALUE?

Dividends are paid in lieu of capital appreciation. Investors can choose from schemes that payoff dividends daily, weekly, monthly, quarterly, yearly, etc.

Dividends paid by the mutual fund schemes may include the dividends received from the stock holdings of the mutual fund portfolio. It also includes the gains booked from the sale of the stock holdings of the scheme. These gains can be partially or wholly distributed at the fund manager’s discretion.

In growth plans, since no dividends are declared, and the gains are accumulated, their NAVs seem to be intact and grow over time. Whenever a growth plan makes gains, the NAV rises automatically. Similarly, when the scheme suffers a loss, the NAV tends to fall.

However, the NAV of IDCW plans tends to grow at a slower pace in comparison with Growth plans as dividends are declared and distributed from time to time.

WHY GROWTH OVER IDCW?

Investors opting for IDCW plans would lose on compounding and wealth creation as the gains are paid out, which might have an impact on the final corpus.

Dividends on IDCW plans are taxable at the hands of the unit holder based on the tax slab rate applicable, whereas growth plans are taxable only during redemption. Moreover, equity and hybrid funds are more tax-efficient in growth plans than dividends.

The returns generated from growth plans would beat inflation, whereas the returns generated from IDCW plans would be relatively low and might not end up beating the inflation rate.

Growth plans promote discipline as the gains are accumulated in the long run.

The opportunity cost of money received as a dividend might be low when compared to the cost of the gains staying invested in the scheme.

IS THERE AN ALTERNATIVE TO IDCW PLANS?

A mutual fund Systematic Withdrawal Plan is an option for investors to get fixed cash flows from their investments. Through SWP, a pre-determined amount can be withdrawn weekly or at any frequency determined by the investor. The withdrawn amount will be directly credited into the bank account on the specified date.

The withdrawal can be initiated as long as there are balance units in your mutual fund scheme account. The unit balance of the scheme will diminish with each SWP installment, but if the NAV keeps increasing at a faster rate than your withdrawal rate, then appreciation can be expected in the value of residual units as well.

SWP VS IDCW

In SWP, investors are in control of the frequency and the value that they would like to withdraw from the scheme, whereas dividend payouts are based on the sole discretion of the fund manager.

Market situations and NAV movements might affect dividend payout frequency, while SWPs can be initiated irrespective of the market and NAV movements.

For investors in the higher tax slabs, SWPs would be a clear winner since the entire SWP proceeds would not be taxed, and only the capital gains portion would be taxable.

TO CONCLUDE...

It is often suggested that investors wanting a regular source of income or cash flows from their investments can opt for IDCW plans. But, SWP seems to have its advantages over IDCW.

And, investors wanting to create and accumulate wealth, in the long run, can go for Growth plans as it outperforms IDCW plans when it comes to tax efficiency, long-term wealth compounding, and maintaining investment discipline.