Taxes are the biggest nightmare for any working person. It does not just eat up one's income but also spoils their overall wealth creation journey. It is a double whammy. Do we have a solution which covers both the problems? Yes!

Section 80-C of Income Tax Act allows any Resident Indian to save up to Rs 1.5 Lakhs under various schemes, which help in reducing the overall taxable income. But do all of them work well when it comes to creating wealth? The answer is a straight No!

There are numerous instruments which facilitate tax saving under section 80-C. The most popular or the most subscribed ones are as follows:

- Public Provident Fund(PPF)

- Investment Linked Insurance Policies (ULIP/Moneyback/Endowment)

- 5 year Bank Fixed Deposits

- Equity Linked Savings Scheme(ELSS)

- National Savings Certificate(NSC)

Let us now look at some core points of comparison:

But all this is just one portion of tax saving under Section 80-C. There is an additional clause which states that another Rs 50,000 can be saved under Section 80CCD(1b) through an instrument which is extremely safe as it is government backed and at the same time, returns are also linked with the market, making it a more lucrative investment option for investors with moderate risk appetite. The product is known as National Pension Scheme(NPS)

National Pension Scheme or popularly known as NPS is a widely subscribed investment product in India and has the highest levels of safety as it is regulated by the Pension Fund Regulatory and Development Authority(PFRDA) and the Union Government. It is primarily used by the majority of adherents as a safe haven, yielding passive income post retirement to meet their routine expenditure.

Suitability and Benefits of NPS:

- Investors who are looking to lock their money till the age of 60

- 60% of the accumulated corpus is withdrawable at the age of 60, which is completely tax free. The remaining 40% is used to purchase an annuity to provide pension in the form of periodic fixed income at fixed intervals

- Returns better than pure government backed schemes like PPF, NSC etc but at a higher risk

- Regular stream of income after retirement in the form of annuity, which can be monthly, quarterly, half yearly or annually

- Exposure to Equity, Debt and Alternates supported by solid fund management with a diversified portfolio

- Flexibility to choose between various asset classes based on risk appetite

- Investments can be started with just Rs 500

- Authorized by PFRDA, making it one of the most secure forms of investments for retirement

- Extremely low fund management charges, as low as 0.01% of the entire investment corpus

- Inculcates financial discipline while saving for retirement as mandatory lock in makes it impossible to withdraw in normal circumstances

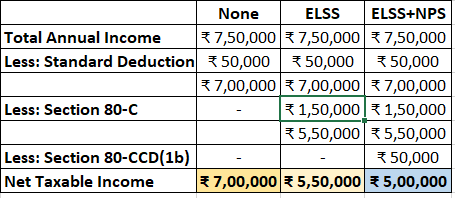

Let us take an example of a salaried resident Indian to understand the effect of tax saving investments. Mr. Khalid, working as a software developer in a private company earns around Rs 7.5 Lakhs per annum. Below table shows the various scenarios of taxable income

It is clearly visible that Mr. Khalid can reduce his taxable income by a massive amount of Rs 2 Lakhs through proper investment planning, helping him save more and also grow more through the invested amount.

Taxation on Maturity:

Insurance Linked Policies like ULIP/Moneyback and Public Provident Fund(PPF) are completely tax free at the time of maturity. Interest on FD and NSC are taxed as per marginal taxation slab rates. ELSS follows taxation based on Long Term Capital Gains, which states that profits up to 1 Lakh is exempted and anything over and above that is taxed at 10%. NPS has two parts. The first part is completely tax free as 60% of the entire corpus can be withdrawn in a single shot. The second part is treated as income as the remaining 40% of the corpus is converted into an annuity, therefore taxed as per marginal taxation slab rates.

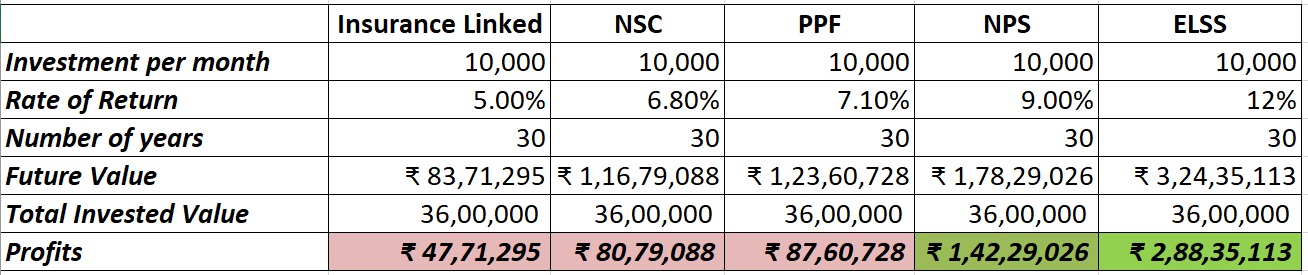

From the above table, there is a clear picture of wealth creation done through tax saving instruments. It is safe to say that ELSS and NPS are most efficient for any individual looking to minimize tax liability and at the same time, helps in maximizing returns to a greater extent as opposed to the other products. The opportunity cost is significant as ELSS can be withdrawn in just 3 years and can be utilized for several other pressing purposes while the other instruments are more prone to be held for a much longer duration, making investors dependent on other avenues for immediate liquidation.

The most appropriate one for covering Rs 1.5 Lakhs under Section 80-C would definitely be ELSS while an additional Rs 50,000 can be grown at a healthy rate by investing in NPS, making it a duo of saving totally Rs 2 Lakhs. Together, one does not just save taxes but also makes sure their wealth is grown at a very healthy rate!

Investors can consult their financial advisors on what will work best for them based on their needs, goals and risk profile. It is important to discuss and arrive at an optimal solution before investing in any of these instruments.